You have submitted an Offer in Compromise to the IRS, with all documentation attached. You are happy that you have taken an ideal step to place your tax issues behind you. You were positive that the Internal Revenue Service will say yes to your proposed offer. Quite the opposite, you just received a formal rejection letter from the IRS notifying you that your Offer was not accepted. You are devastated!

The Internal Revenue Service usually rejects most Offer in Compromise applications for numerous reasons; in fact, less than 30% of all OICs submitted were accepted by the IRS. Let's talk about the reasons why the IRS will reject an offer and what are the things you need to stay away from.

1. When you didn’t substantiate

An Offer in Compromise is a legal claim where each supporting documents you send out will count towards the success of your application. The Offer in Compromise procedure will not be like a income tax return where 99% of this will never go for an IRS audit.

But in Offer in Compromise, you'll find certainly an IRS person who will scrutinize the data you entered on the form 656 Offer in Compromise and the Collection Information Statement. The examiner might request you to send even more additional documents like the bank statements, vehicle registrations, property details, and a multitude of other things to substantiate the information.

2. Not staying current in tax filing/payment

Should the IRS knows you won’t stay current with your offer, there is no reason at all for them to accept an offer. There’s a mythos that the IRS’s “Fresh Start” program will make your tax debt magically go away. However the IRS Fresh Start OIC Program is only a set of guidelines that cannot - wait for it, an lawyer word is here - ameliorates your responsibility to stay in current compliance with your filing & payment requirements.

3. Not rebutting IRS’s claims

Nobody is perfect and IRS examiners too make mistakes. An examiner can “mistakenly” misestimate or misrepresent your submission. If you notice any fault in computations, you've got full right to refute the examiner.

And too often taxpayers (or their spokes people) simply just roll over and accept plain error rather than remark obvious mistakes an OIC Examiner made when computing your Reasonable Collection Potential (RCP).

4.You didn’t move to the appeals division

Are you aware of, you've got the legal right to appeal the IRS decision? If at first you don’t succeed, appeal. But get this - your appeal will only be as good as your underlying offer. Therefore , avoid the above mistakes and utilize best practices to boost your chances of your offer acceptance.

As 2015 filing season has started, it is time for the taxpayers to be aware of latest tax rules changes and in what ways it'll impact federal tax returns for the 2015 tax period. I'm going to look into pinpointing 3 areas that our clients should be aware of.

2015 Tax Rate and Capital Gains Tax Changes

The top tax rate of 39.6 % will hit individuals with incomes of $413,200 and above for single adult and $464,850 for married citizens filing a joint return. This is up from the 2014 standards of $406,750 and $457,600, respectively.

The capital gains tax rate stays at 0% for citizens inside the 10% and 15% tax brackets and the 15% rate for all of the other tax brackets. But for people in the 39.6% tax bracket, 20% long-term capital gains tax rate will apply from now on applied. Standard deductions increase to $6,300 for single filers, up from $6,200 for 2014 and $12,600 for married joint filers in 2015. The personal exemption for tax year 2015 increased $50 to $4,000.

Retirement Savings Changes For 2015

For anyone looking to gain the best from their existing 401(k), the laws will permit individual contributions of $18,000 to 401(k) plans in 2015. The catch-up contribution limit are likewise increased by $500 for individuals who are 50 years or older .

.jpg?timestamp=1429342102299)

The most significant change in the law is the new rollover limitation. Beginning on January 1, 2015, taxpayers can perform just one tax free rollover from one IRA to another IRA in a 12 month period. A rollover is known as distribution from one retirement plan that you make a contribution to another retirement plan. Prior to 2015, people were able to exclude carry over distributions from one IRA to another IRA from their gross income if the same was transferred into another plan within sixty days. This enabled individuals to essentially take penalty free, tax-free and interest free loans from one's retirement accounts. Sadly, the new change in the tax law restricts people from having such tax-free IRA financial loans.

On the other hand, this new rule will not apply to trustee-to-trustee IRA fund transfers or traditional to Roth IRA conversions. This direct rollover transfer method enables investors transfer cash amongst IRA accounts without taking control of the money. This fund transfer is tax-free and will not set-off the 10% early withdrawal penalty. Contact a tax attorney if you have several retirement accounts and planning an IRA distribution but not confident about whether it falls inside the one per 12 month limit or not positive on doing tax free IRA transfer.

Affordable Care Act Changes for the tax year 2015

Among all tax law changes this year, The Affordable Care Act (ACA) stands out as the biggest single change which has ever happened to the tax code in 20 years. The individual mandate requires most Americans with income over particular thresholds to have or obtain health insurance if not insured by federal/state government programs. If individuals do not have employer sponsored health coverage, they need to obtain their very own private insurance or get protected under state run exchanges starting in 2014.

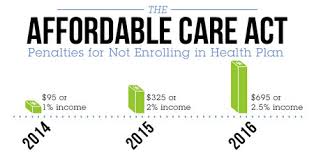

Those individuals who failed to get health insurance will have to fork out non-compliance penalty to the IRS starting this present year. For example, the non-compliance penalty for the 2014 tax period is $95 per individual and up to $285 for a household or one percent of income, depending on whichever is greater. The penalty is slated to go up considerably in 2015: to a $325 minimum per individual or 2 percent of income, whichever is higher. In the year 2016, it will get even worse as the penalty will jump drastically to $695 per individual and around $2,085 for a family or 2.5% of household income, whichever is greater.

Small-business proprietors obtaining health insurance via the Small Business Health Options Program (SHOP) Marketplace can receive tax credits and tax breaks. If your company employs only 25 full-time workers with average annual paycheck less than $50,800, you can access the program to offer health insurance to staff members and additionally get tax benefits. Pertaining to ObamaCare's employer mandate, companies with over 100 full time employees will need to provide health coverage to at least 70% of employees beginning in 2015. This rule will not impact organizations with 50 to 99 full time employees up to Jan 1, 2016.

Having an Offer in Compromise accepted is not automatic. It is actually quite difficult however, if done correctly, you may qualify for acceptance. Indeed, it can be achieved.

Even if you're qualified to apply for an offer in compromise, no one can guarantee that your offer will be accepted. Any tax law firm that guarantees that the IRS will accept your Offer in Compromise isn't representing your best interests. We do not guarantee because we can’t guarantee. On the other hand, following are the things you should do to increase your odds of having your Offer in Compromise approved by not taking oneself out of the game.

Are you filing and paying out your taxes on-time? If running your own business, have you completed making payment on the latest estimated quarterly tax? If you are a w -2 employee, is the withholding correct? Otherwise, the internal revenue service will decline your OIC as you have demonstrated that you cannot follow the tax compliance rules.

.jpg?timestamp=1403982220369)

You need to have filed all the income tax returns. Once Again, how is the government expected to do you a big favor and reduce your taxes with an Offer in Compromise if you are simply letting them know you will do your taxes your way and not their way? You must be tax compliance. Compliance would mean you do things the way they say( which can be unquestionably challenging, especially when you can’t fully grasp them).

Do you have presented the whole set of documentation to the Internal Revenue Service? Dealing with the IRS sentimentally or shouting at them will never work.

Did you submit all required payments? If you don’t send in your fee or fee waiver, the IRS won't be able to process your Offer.

Be truthful with all the information you present to the IRS. Integrity is key here. The IRS usually selects a taxpayer's file for further scrutiny when they discover any type of suspicious activity within the information they provided. Giving fraudulent information in an OIC form is definitely a serious crime with adverse consequences and a crime that rarely remains hidden.

Do you think you're being polite and respectful to the IRS Offer in Compromise Examiner? Don't complicate things by treating IRS examiner in a impolite manner. They could make your life miserable. The end result will be better if you are respectful and friendly to the authorities, recognizing that he or she is just trying to do the job. But try not to go overboard. Stick to respectful, courteous and professional. An examiner's mission is usually to efficiently process each assigned case, so prompt co-operation can improve the chances of a satisfactory conclusion. If you can't give good response, the risk of your OIC getting denied will simply get higher and higher.